Q3 Earnings and Sector Performance

We delve into the Q3 earnings and how pre-season expectations have panned out in reality

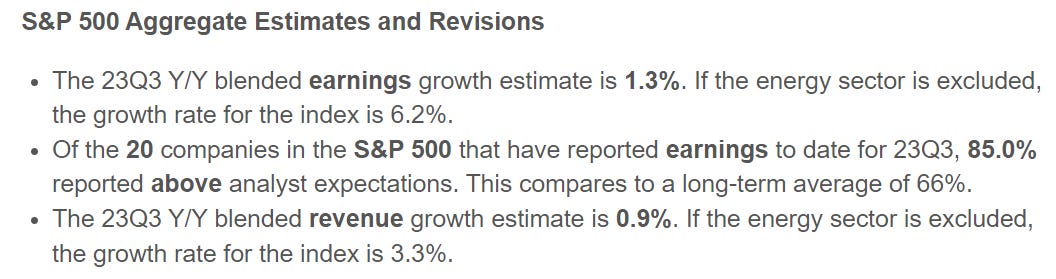

One month into the earnings season, 80% of S&P500 companies have reported already and it’s time to take a look at how they have fared Y/Y and against expectations.

Let’s start with how the season was supposed to play out. We use data from Refinitiv and the dashboard they prepare during the earnings season is the best there is. We always acknowledge the source of the data and author Tajinder Dhillon.

The analysts were expecting good Q3 with small growth in revenue and a decent growth in earnings save for the Energy sector (mostly due to tough compares Y/Y).

It was pretty clear from the first big week that the numbers were going to be better than expected. Only the scale of outperformance remained to be discovered. So with 90% of S&P500 market-cap behind us, what does the earnings picture look like?

You can see the numbers above. The biggest of the companies are in good shape and continue to report strong earnings and decent revenue growth. I have always called out the importance of paying attention to data and not the narrative. This is the reason why that is important. Let’s get deeper into the numbers to see what the sectors have done.

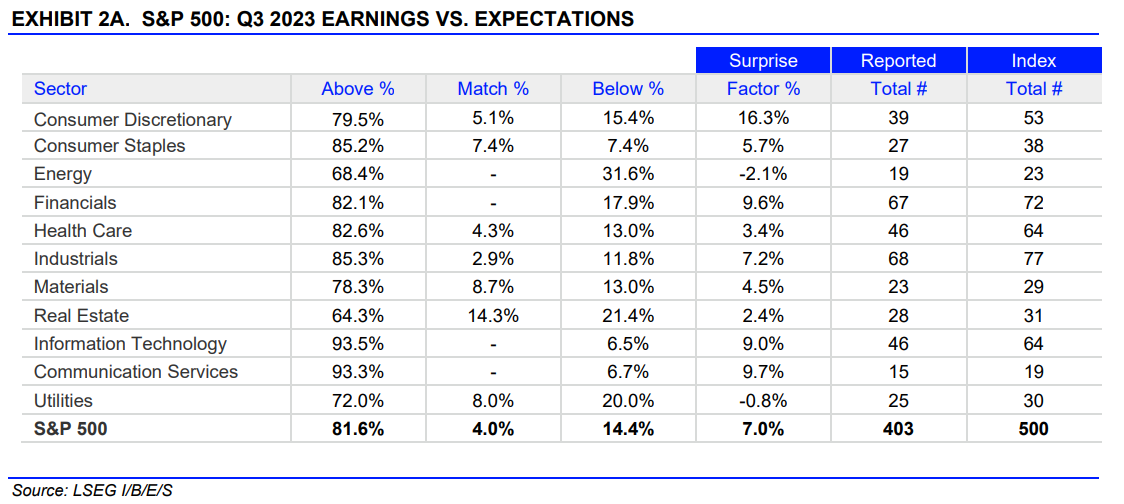

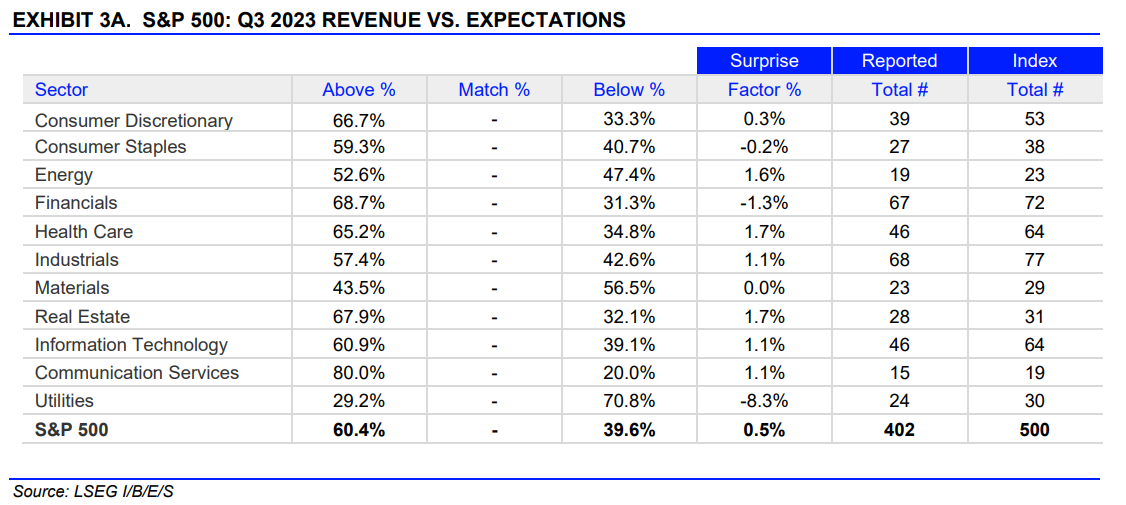

Both in Revenue and Earnings, the percentage beats are above long term averages

Clearly the earnings growth is outstripping revenue growth. Does this really imply that the cost cutting is the reason for the good earnings? Yes and No of course. Again beware of the narrative that is not supported by data. If you go into each company report and see the commentary on earning Y/Y, you will see staff reductions, cost cuts in programs, efficiencies, better management of spend in relation to updated economic outlook and many more factors. This is normal part of management activities. Some of it is short term benefit while others are sustainable for a long time. The point is to understand each of those and how they play into the stock valuation short and long term. Also don’t discount the revenue growth we are seeing in Q3 and the guidance for Q4.

Taking a quick look at our own thoughts early in October:

Big Banks had very good earnings but trade currently below their post earnings price. We have not changed our opinion on big banks. We still like JPM, MS and GS.

Energy sector we said that expectations were too negative. We were correct, the sector has performed slightly better. We still like Big oil and continue to hold our positions

Communication Services: We we absolutely right on Ad Spend growth rates moving up. While Google sold off, we expect it to reverse into a strong Q4. We still like this sector to outperform. The data was confirmed by earnings from other companies in the space

Consumer Discretionary: Our take on AMZN was very accurate. Big beat on Ad revenue, retail margins jumped on cost control and mix and string consumer, AWS was not a disappointment. We still like AMZN in Q4.

Technology: MSFT positive surprise was something I did not expect this quarter. That has blown away expectations. Apple was at best neutral with a drag from China. SaaS & Cybersec has been negative for smaller players. We still expect the leaders to beat and guide up. In technology the Q4 play is sector leaders with a breadth of product portfolio and significant moat in their strong product line. We again like MSFT’s quarter not its valuation.

Healthcare is again playing out exactly as predicted. NVO and LLY are big winners and continue their growth. Others that were sold of on potential GLP-1 impact are recovering.

Industrials: This is also in line with our take, Book to Bill ratios are strong in Defense. We see some headwinds with budget fight in Congress. However we thing the re-rate of Defense is around the corner as capacity addition is fully utilized and Worldwide defense spend keeps going up.

Materials: China continues to buy Iron Ore so the big moners are doing well. Copper market is also stabilizing.

Utilities has outperformed earning expectation and the stocks have done well in the recent pullback

We have much more work to do on Staples & Real Estate before we can express any definitive opinion on the sectors.

We will leave you with a look at the sector Weekly Chart. We still like XLC to continue strength in Q4. We are also watching the trend reversals in the safety sectors: SLU, XLV and XLP

We will go deeper into this in the next article in a couple of weeks. We will also start looking Q4 expectations.

If you like these post please follow @MonetiveWealth and @Archna2011 on Twitter. As always, these are our thoughts on the market. Please conduct your own due diligence and consult an licensed financial advisor before you commit your capital..